Private Exclusive Legislation: How States Are Rewriting the Rules of Listing Visibility

A trend that started in Wisconsin in late 2025 has, in the span of about six months, become the most active area of real estate regulation at the state level since Sitzer/Burnetts.

A private listing used to be an internal industry problem. An MLS could write a rule, a brokerage could object, NAR could clarify the policy, and the argument mostly stayed inside the real estate profession. That boundary is breaking down. Over the last six months, state legislatures have started converting the private exclusive debate into licensing law, which changes both the stakes and the forum. Once a question moves from the MLS rulebook to the statute book, the industry no longer gets to settle it by committee.

The technical language changes by state: private listings, office exclusives, pre-marketing, pocket listings, private listing networks. The policy question underneath is the same. When a licensed broker takes a residential listing, how much control should that broker have over who gets to know the property is available?

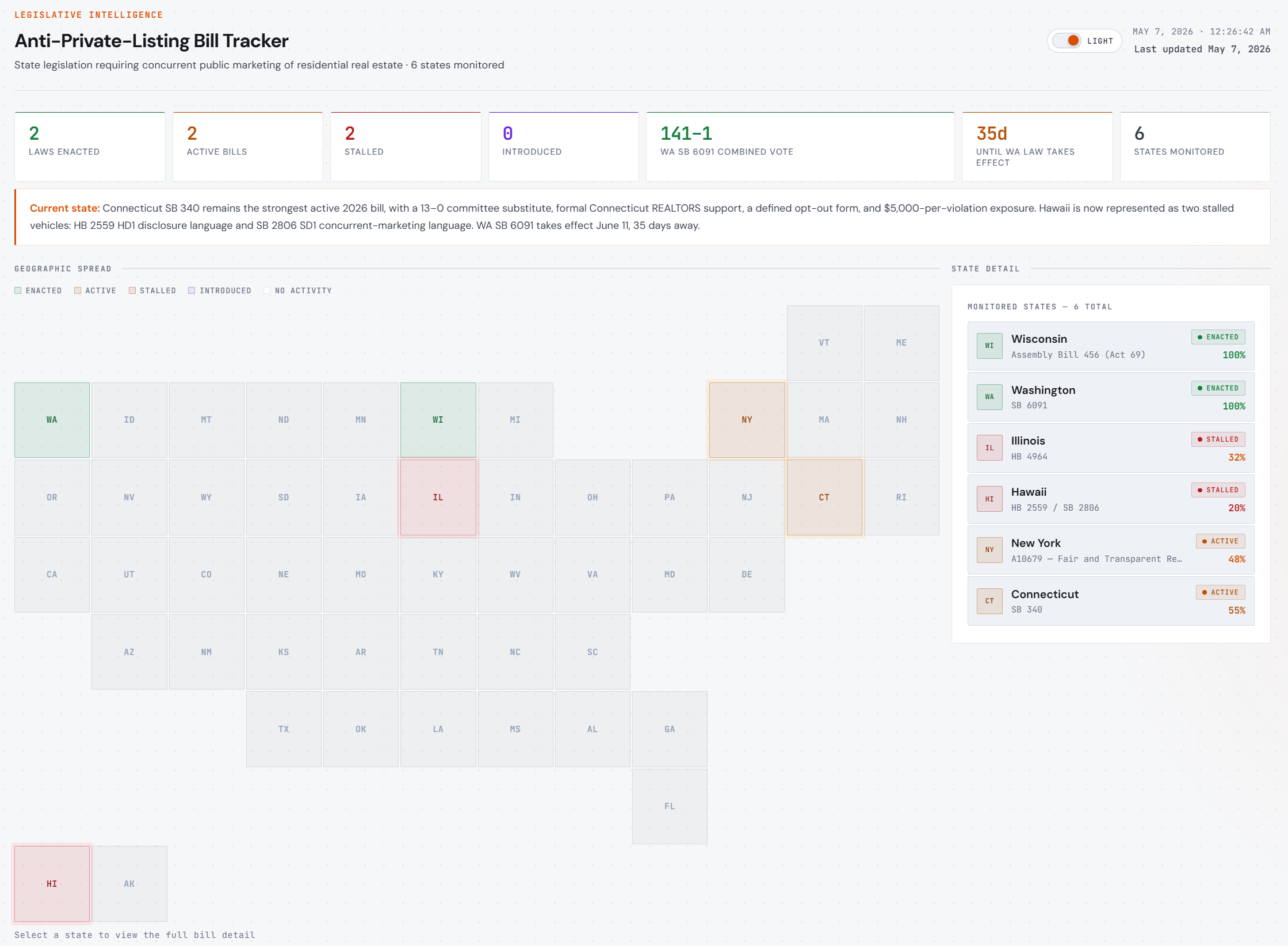

I started tracking this because the movement was spreading faster than the industry conversation around it. The dashboard at legtracker.cooperthayer.com tracks the bills by state, bill number, sponsor, status, and policy model. It also separates the two structures that now define the national debate: the Wisconsin model, which allows private marketing after a seller signs a disclosure and opt-out form, and the Washington model, which requires concurrent public marketing whenever the property is marketed to any limited or exclusive group.

Two Different Models

Wisconsin and Washington are easy to group together because they are the two states to have successfully enacted private listing legislation. That grouping is useful for a map, but it is not useful for understanding the policy. The two laws are built on different theories of regulation, and the difference is important because other states are now choosing between them.

Wisconsin treats the issue as a disclosure and consent problem. Under 2025 Wisconsin Act 69, which takes effect January 1, 2027, a listing firm handling 1-4 unit residential properties must share information with buyer-side licensees, respond to inquiries, make the property available for showings, and publicly advertise or market the property within one business day of the listing agreement unless the owner signs a state-prescribed disclosure and opt-out form. The law does not eliminate private marketing. It makes the seller’s decision formal, documented, and tied to a state-mandated warning about the possible trade-offs of restricted exposure. (Wisconsin Legislature Docs)

Washington starts from a different premise. SB 6091, signed by Governor Bob Ferguson on March 16, 2026, and effective June 11, 2026, prohibits a broker from marketing residential real estate to a limited or exclusive group of buyers or brokers unless the property is concurrently marketed to the general public and all other brokers, with only a narrow exception for health or safety concerns. The bill passed 49-0 in the Senate and 92-1 in the House, which is part of why it matters beyond Washington. It was a landslide, not a marginal partisan bill that slipped through on a narrow vote. (Washington State Legislature)

The difference in ideology is substantial. In Wisconsin, a private-first strategy can survive if the seller signs the required opt-out and the file supports the decision. In Washington, the sequence itself is the regulated conduct. A broker cannot expose the property first to a brokerage network, preferred buyers, selected agents, or a private channel and then open the market later, unless the health or safety exception applies. Wisconsin regulates the decision to restrict exposure. Washington regulates the act of restricted exposure by a licensed broker.

Seller Consent vs. Broker Conduct

The Wisconsin model assumes seller consent can solve enough of the market-access problem to justify allowing private marketing in some cases. The mechanism is familiar: disclose the risk, document the client’s instruction, preserve the file, and allow the professional to proceed if the client chooses that path. It is the same regulatory logic behind many existing real estate disclosures. The state does not say the conduct can never happen. Rather, it says the seller must be told what the conduct may cost before the broker relies on that instruction.

The Washington model assumes disclosure is not enough. It treats broker-controlled restricted exposure as a market-access problem that cannot be cured by a signed form, because the harm is not limited to the seller who chose the private process. Buyers outside the selected channel lose access. Buyer agents outside the selected channel lose visibility. Competing brokers operate with incomplete information. Pricing information becomes less reliable when a larger share of inventory trades through selective distribution.

“These private listing models that are growing in popularity aren’t just a threat to consumer protections — they’re a way of excluding some people from being able to buy or rent homes in our state. This bill is fundamentally about fair housing. When buyers and renters have equal access to the market, we level the playing field so everyone can consider all available options when they’re searching for their next place to call home.”

- WA State Sen. Marko Liias (Washington State Senate Democrats)

Other Bills Now in Motion

The rest of the legislative map is beginning to organize around those two templates.

Illinois’ HB 4964 follows the Wisconsin structure. The bill would require a listing licensee to share information with buyer-side licensees, respond to inquiries, make the property available for showings, and publicly advertise or market the property within one calendar day of the brokerage agreement unless the seller signs a disclosure and opt-out form prescribed by the Department of Financial and Professional Regulation. (LegiScan)

Connecticut SB 340 also tracks closer to Wisconsin than Washington. The bill establishes requirements for public marketing of certain real estate listings and creates an opt-out structure rather than a flat concurrent-marketing mandate. As of early May 2026, LegiScan shows the bill passed both chambers unanimously, with a 36-0 Senate vote and a 149-0 House vote. (Connecticut General Assembly)

Hawaii SB 2806 is closer to Washington. It would prohibit brokers from listing or offering residential real estate to a limited or exclusive group of prospective buyers, brokers, or salespersons, with limited exceptions, and would treat violations as unfair or deceptive trade practices and grounds for discipline. The bill passed the Senate and was referred to the House Consumer Protection and Commerce Committee. (LegiScan)

New York’s A10679, the Fair and Transparent Real Estate Listings Act, is more of a hybrid, though it leans toward the Wisconsin side because it allows non-public marketing after informed written seller direction. The bill is also worth watching for its definitions. It gives one of the clearer statutory treatments of a private listing network, and definitions can spread before full policy structures do. (New York State Senate Legislation)

The Industry Never Settled the Question

The statehouse activity is happening because the industry never reached a stable settlement on listing access. NAR’s Clear Cooperation Policy remains in place, but in March 2025 NAR added Delayed Marketing Exempt Listings through its Multiple Listing Options for Sellers policy. Sellers can now direct their listing broker to delay IDX and syndication for a locally defined period while the listing remains filed with the MLS and available to MLS participants. NAR also clarified that one-to-one broker communications do not trigger Clear Cooperation, while multi-brokerage communications do. (Washington State Legislature)

That compromise gave the industry another category, but did not resolve the underlying conflict. Compass has continued to defend and market its private exclusive and pre-marketing strategy, and its February 2025 analysis reported that Compass pre-marketed listings were associated with a 2.9% higher final close price compared with Compass listings that went directly to the MLS, based on a hedonic regression of 2024 Compass sell-side transactions. (Compass)

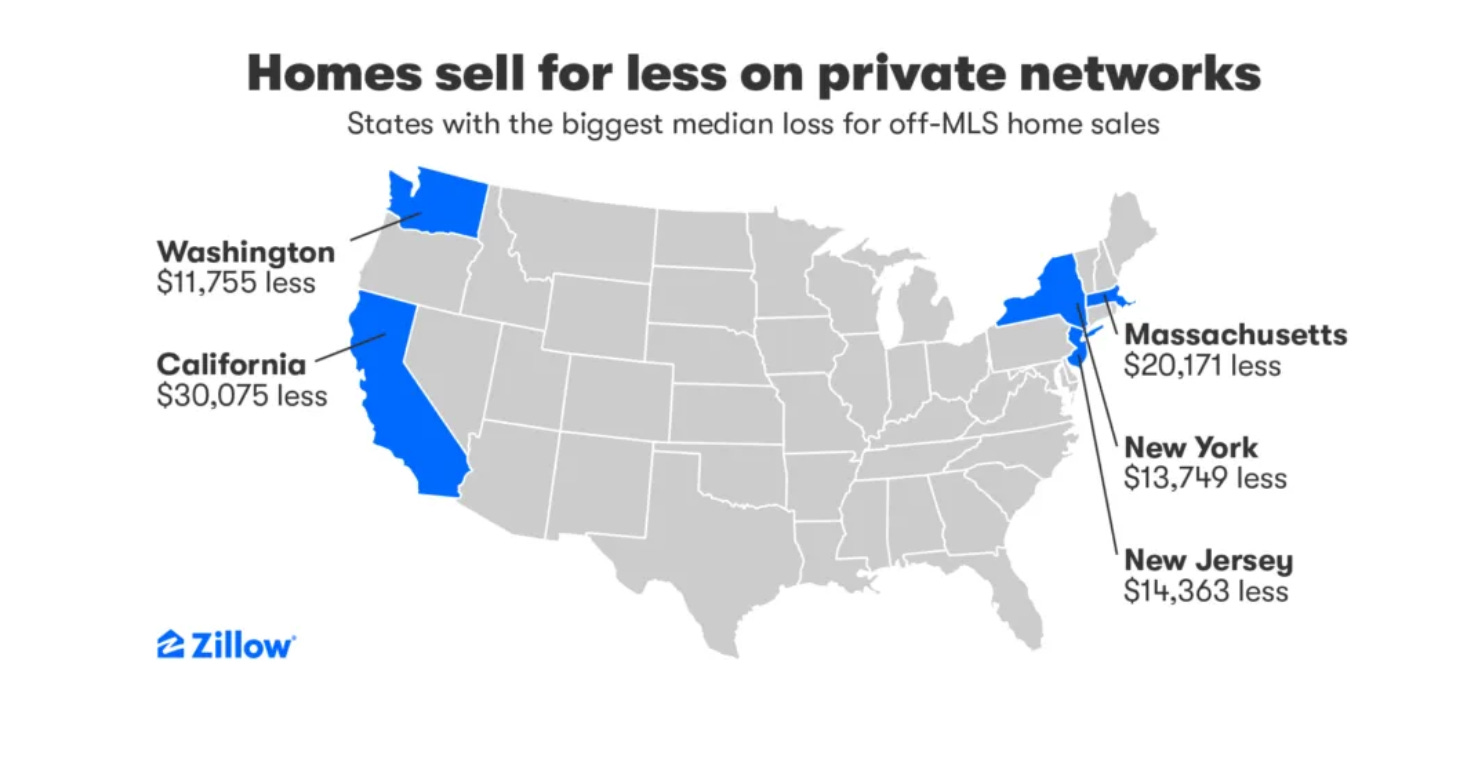

Zillow and Bright MLS point in the opposite direction. Zillow’s February 2025 study found that homes sold off the MLS in 2023 and 2024 typically sold for $4,975 less nationally, with California showing a reported median gap of $30,075. Bright MLS, working with Drexel University, found a 17.5 percent on-MLS premium across more than one million Mid-Atlantic transactions from 2019 through Q1 2023. (Zillow)

Those studies should not be treated as if they measure the same thing. Compass is studying its own pre-marketed listings that later moved through its system. Zillow and Bright are studying broader off-MLS outcomes. Different populations can produce different results without either side necessarily fabricating the conclusion. Data can be accurate, yet still misleading.

This Is Not Really NAR Versus Brokerages

The lazy version of this story is NAR versus Compass, MLSs versus brokerages, or portals versus private networks. Those disagreements may exist, but they are too narrow to explain why legislators are now interested. The better frame is transparent market ideology versus seller-directed control.

The transparent-market argument starts with access. A residential market works better when buyers, buyer agents, appraisers, brokers, and data systems can see available inventory. Broad exposure improves price discovery, makes comparable sales more reliable, and reduces the chance that access depends on brokerage affiliation rather than buyer qualification.

The seller-control argument starts with agency. Some sellers have legitimate reasons to avoid full public exposure, at least for a period of time. Privacy, security, timing, price testing, and time-on-market stigma are legitimate concerns. A seller with a public-facing job, a complicated family situation, or a property that is not ready for photography may have reasons to prefer a narrower process.

However, the challenging case is not a seller who wants privacy. Rather, it’s a brokerage model that turns seller privacy into an inventory distribution and marketing strategy. A seller choosing not to blast a home across the internet is distinct from a brokerage building a restricted listing channel around that choice.

The Seller Choice Argument Misses the Licensing Issue

A lot of the public commentary describes these bills as restrictions on seller choice. The argument is simple: the seller owns the property, so the seller should decide how it is marketed. I’d argue that framing sounds stronger than it is because it ignores the licensing implications.

A seller remains free to sell privately. They can skip the broker entirely, call a neighbor, hire an attorney, advertise through their own network, or run a narrow process without entering a licensed brokerage relationship. These bills do not create a general obligation for every homeowner to advertise publicly. They only regulate what a licensed broker may do after taking the listing.

Real estate licensing law already limits broker conduct in ways that sellers cannot waive casually. Advertising rules, agency duties, disclosure requirements, fair housing obligations, supervision standards, and trust-accounting rules all exist because the state has decided that licensed brokerage is not just private contract work. It is a regulated profession.

The cleanest critique of the seller-choice argument is that these bills restrict broker choice, not seller choice. The seller can choose not to use a broker. Once the seller hires one, the state can decide what obligations attach to the license. A serious opposition argument would say the state is overcorrecting, that informed consent should be enough, or that privacy cases are too varied for a statutory default. Those may be valid arguments, but they are certainly stronger when made as arguments about brokerage regulation, not as arguments that these bills prevent private owners from selling quietly.

Where the Wave Likely Goes in 2027

The next stage will not be measured only by how many bills pass, but by which model spreads. If Connecticut is signed into law, the Wisconsin structure gains another proof point because it is the easier political sell. Legislators can say they are not banning private listings; they are requiring disclosure, consent, and a public default. That gives state associations room to support transparency without telling every seller that privacy is unavailable.

Washington creates a different kind of momentum. Its vote margins were overwhelming, and the bill’s simplicity will appeal to lawmakers who do not want to litigate whether each opt-out was truly informed. A concurrent-marketing rule is easier to explain, easier to enforce, and harder for a brokerage to route around through paperwork.

My expectation is that private exclusive regulation bills appear in at least five to ten additional states during the 2027 sessions. California is the most important state to watch because the market is large, the luxury segment is visible, Compass has a significant market share, and the consumer-finance argument is easy to make after Zillow reported a $30,075 median off-MLS gap in the state.

Florida is less predictable because the legislature is not naturally inclined toward more licensing regulation, but the state has high transaction volume, large relocation markets, and enough luxury activity to make private marketing a live issue if the national conversation accelerates.

Texas is the wildcard. TREC and Texas Realtors have a long history of shaping licensing rules without much public drama, and the state’s major metros are large enough that a Texas bill would immediately change the national conversation.

Smaller states may move first because the politics are easier and the state associations can act more quickly. Massachusetts, New Jersey, Oregon, Maryland, Virginia, Minnesota, and Colorado are all plausible places for 2027 activity if the Wisconsin and Washington templates keep traveling. The precise state list will depend less on ideology than on who brings the bill, whether the state association supports it, and whether the language looks like disclosure policy or a private-network ban.

What’s Next?

The next year will clarify whether this becomes a broad licensing trend or a short burst of state-level experimentation. Connecticut is the first signal. If the bill is signed, the opt-out structure becomes the more politically proven model, especially for states that want to preserve seller-directed privacy while still regulating broker conduct.

California is the second signal. A California bill would not need to pass immediately to change the conversation. Introduction and consideration alone would force every national brokerage, portal, MLS, and state association to decide whether this is now a defensive issue or an offensive one.

Model language is the third signal. A wave of Wisconsin-style bills means legislators are prioritizing informed consent and file documentation. A wave of Washington-style bills means legislators are prioritizing concurrent access over private sequencing.

The industry spent years treating private listings as an MLS policy problem. State legislatures are turning it into a licensing problem. Once that happens, the debate stops being about which platform, MLS, or brokerage has the better rule and starts being about what the state expects from a licensed professional.

Wisconsin says a seller can opt out after disclosure. Washington says a broker cannot create exclusive access unless public access happens at the same time. Those are not variations of the same policy… they are competing theories of how much control a licensed broker should have over market visibility.

Track the legislation and latest news at: legtracker.cooperthayer.com

See something that I missed that should be included? Email me!